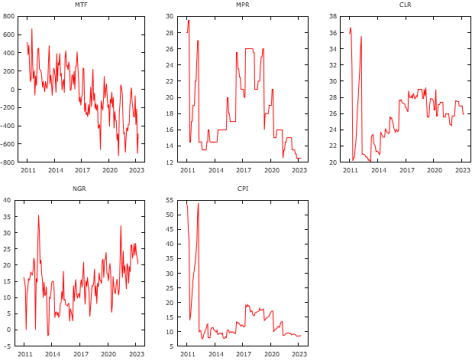

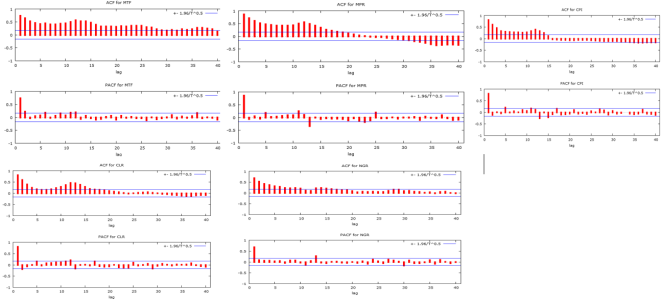

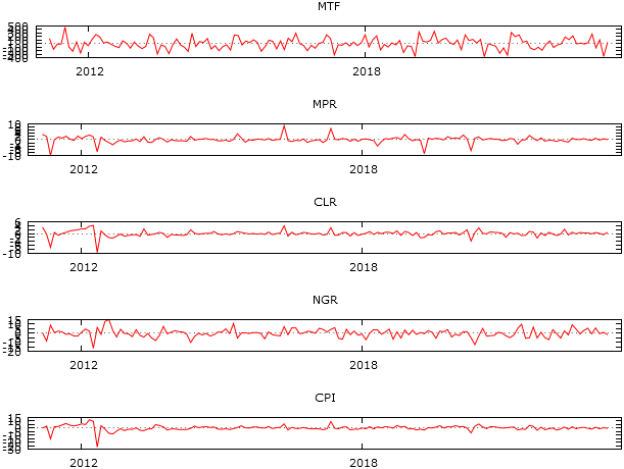

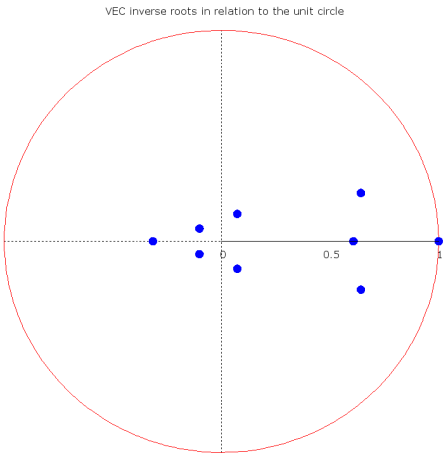

Macroeconomic variables serve as economic indicators that offer valuable insights into the overall health and stability of an economy. Changes in these variables can have significant impacts on a country's trade balance and overall economic performance. This study employed multivariate time series analysis to study the relationship between Merchandise Trade Flows (MTF), Monetary Policy Rate (MPR), Commercial Lending Rate (CLR), Nominal Growth Rate (NGR) and Consumer Price Index (CPI) with Money Supply (MoS) as exogenous variable. The nature of trend in each series was investigated. The results revealed that quadratic trend model best models MTF, MPR, CLR and NGR whiles an exponential trend best models CPI. Johansen’s co-integration test with unrestricted trend performed revealed the existence of long-run equilibrium relationships between the variables and three (3) co-integrating equations described this long-run relationship. In terms of short-run relationships, the VEC (2) model revealed that, CLR, NGR, MoS have positive and significant impact on MTF. CLR, NGR and MoS have positive and significant impact on MPR, NGR have positive and significant impact on CLR, CPI and MoS have significant impact on NGR whiles NGR and MoS have significant impact on CPI. Model diagnostics performed on the VEC (2) model showed that, all the model parameters are structurally stable over time and the residuals of the individual models are free from serial correlation and conditional heteroscedasticity. Forecast error variance decomposition (FEVD) analysis showed that each variable primarily explained its own variance and the influence of other variables increase over time. Hence, adopting a broad perspective on macroeconomic variables can help policymakers anticipate and mitigate ripple effects across various economic sectors.

| Published in | American Journal of Theoretical and Applied Statistics (Volume 13, Issue 5) |

| DOI | 10.11648/j.ajtas.20241305.15 |

| Page(s) | 157-174 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2024. Published by Science Publishing Group |

Macroeconomic Variables, Merchandise Trade Flows, Co-Integration

Variable | Mean | Minimum | Maximum | Std. Dev. | C.V. | Skewness | Ex. Kurtosis |

|---|---|---|---|---|---|---|---|

MTF | -31.576 | -733.06 | 666.99 | 275.66 | 8.73 | -0.2129 | -0.2451 |

MPR | 18.25 | 12.5 | 29.5 | 4.541 | 0.2488 | 0.7668 | -0.6195 |

CLR | 25.826 | 20.04 | 36.64 | 3.2464 | 0.1257 | 0.4921 | 1.1448 |

NGR | 14.208 | -1.71 | 35.5 | 6.6288 | 0.4665 | 0.1982 | 0.3439 |

CPI | 14.426 | 7.5 | 54.1 | 9.1239 | 0.6325 | 2.8007 | 8.0285 |

Variable | Model | MAPE | MAD | MSD |

|---|---|---|---|---|

Linear | 323.200 | 151.800 | 34099.00 | |

MTF | Quadratic | 314.3000 | 151.500 | 3384.800 |

Linear | 20.861 | 3.801 | 19.709 | |

MPR | Quadratic | 17.485 | 3.274 | 17.124 |

Exponential | 19.751 | 3.705 | 20.012 | |

Linear | 8.817 | 2.268 | 9.636 | |

CLR | Quadratic | 8.729 | 2.249 | 9.629 |

Exponential | 8.497 | 2.217 | 9.701 | |

Linear | 56.815 | 4.819 | 38.328 | |

NGR | Quadratic | 47.150 | 4.068 | 30.035 |

Linear | 40.287 | 5.658 | 69.785 | |

CPI | Quadratic | 44.685 | 6.006 | 63.084 |

Exponential | 32.840 | 5.233 | 74.133 |

ADF Unit Root test (12 lags) | ||||

|---|---|---|---|---|

Variable | Constant only | Constant and Trend | ||

Test statistic | p-Value | Test statistic | p-Value | |

MTF (Original series) | -0.8687 | 0.7986 | -2.3151 | 0.4251 |

1st differenced MTF | -7.6401 | <0.0001** | -7.5943 | <0.0001** |

MPR (Original series) | -1.1401 | 0.7017 | -1.1570 | 0.9178 |

1st differenced MPR | -3.4767 | 0.0086** | -3.5072 | 0.0385** |

CLR (Original series) | -1.3726 | 0.5974 | -2.3310 | 0.4164 |

1st differenced CLR | -5.0202 | <0.0001** | -50669 | 0.0001** |

NGR (Original series) | -1.1759 | 0.6872 | -1.8865 | 0.6615 |

1st differenced NGR | -5.8661 | <0.0001** | -5.9920 | <0.0001** |

CPI (Original series) | -3.5285 | 0.7315 | -3.2808 | 0.6939 |

1st differenced CPI | -4.1963 | 0.0007** | -4.3932 | 0.0022** |

Lag | Loglik | AIC | SBIC | HQIC |

|---|---|---|---|---|

1 | -1771.9251 | 27.7219 | 29.0145 | 28.2942 |

2 | -1512.5619 | 26.9496 | 28.3837 | 27.9908 |

3 | -1752.0876 | 27.8186 | 29.5832 | 28.5356 |

4 | -1707.1104 | 27.8796 | 30.1947 | 28.8197 |

5 | -1694.3071 | 28.0663 | 30.9338 | 29.2314 |

6 | -1684.3000 | 28.2969 | 31.7159 | 29.6862 |

7 | -1665.1287 | 28.5666 | 32.3570 | 29.9999 |

8 | -1651.8321 | 28.6187 | 33.0885 | 30.4040 |

9 | -1625.5164 | 28.5793 | 33.6197 | 30.6079 |

10 | -1605.2154 | 27.9625 | 34.2434 | 30.9042 |

11 | -1577.6570 | 27.8013 | 34.7556 | 31.0889 |

12 | -1512.7228 | 27.9624 | 34. 6901 | 30.6962 |

Rank (r) | Eigenvalue | Trace test | p-value | L-max test | p-value |

|---|---|---|---|---|---|

0 | 0.3227 | 146.2900 | <0.0001 | 56.8890 | <0.0001 |

1 | 0.25518 | 89.4020 | <0.0001 | 43.0140 | <0.0001 |

2 | 0.1837 | 46.3890 | 0.0002 | 29.6350 | 0.0017 |

3 | 0.0789 | 16.7540 | 0.0530 | 11.9500 | 0.1129 |

Equations | Variables | Coefficient | Std. Error | t-ratio | p-value |

|---|---|---|---|---|---|

Const. | -29.1365 | 260.8600 | -0.1117 | 0.9112 | |

MTF lag 1 | -0.2039 | 0.0820 | -2.4868 | 0.0141** | |

MTF | MPR Lag 1 | -6.1773 | 9.9100 | -0.6233 | 0.5341 |

CLR Lag 1 | 31.3301 | 17.0353 | 1.8391 | 0.0681* | |

NGR Lag 1 | 7.3060 | 3.0953 | 2.3603 | 0.0197** | |

CPI Lag 1 | -3.7180 | 6.6421 | -0.5598 | 0.5766 | |

MoS | 0.0026 | 0.0010 | 2.4963 | 0.0137** | |

EC 1 | -0.3817 | 0.0741 | -5.1496 | <0.0001** | |

EC 2 | -0.5214 | 2.4833 | -0.2099 | 0.8340 | |

EC 3 | 1.8751 | 10.5236 | 0.1782 | 0.8588 | |

R² Adjusted | 0.2594 | ||||

Durbin-Watson | 1.9951 | ||||

Const. | -0.9792 | 3.3993 | -0.2881 | 0.7737 | |

MTF lag 1 | 0.0006 | 0.0011 | 0.5523 | 0.5816 | |

MPR Lag 1 | -0.2630 | 0.1291 | -2.0367 | 0.0436** | |

CLR Lag 1 | 0.5587 | 0.2220 | 2.5168 | 0.0130** | |

NGR Lag 1 | 0.0865 | 0.0403 | 2.1439 | 0.0338** | |

MPR | CPI Lag 1 | -0.0311 | 0.0866 | -0.3589 | 0.7202 |

MoS | 0.0001 | <0.0001 | 1.7873 | 0.0761* | |

EC 1 | -0.0023 | 0.0010 | -2.3405 | 0.0207** | |

EC 2 | 0.0820 | 0.0324 | 2.5327 | 0.0125** | |

EC 3 | -0.0300 | 0.1371 | -0.2188 | 0.8271 | |

R² Adjusted | 0.1259 | ||||

Durbin-Watson | 2.0013 | ||||

Const. | 5.4913 | 2.5493 | 2.1540 | 0.0330** | |

MTF lag 1 | 0.0009 | 0.0008 | 1.1795 | 0.2403 | |

MPR Lag 1 | -0.1147 | 0.0968 | -1.1847 | 0.2382 | |

CLR Lag 1 | 0.2915 | 0.1665 | 1.7512 | 0.0822* | |

CLR | NGR Lag 1 | 0.0768 | 0.0302 | 2.5389 | 0.0123** |

CPI Lag 1 | 0.0049 | 0.0649 | 0.0757 | 0.9398 | |

MoS | <0.0001 | <0.0001 | -0.2929 | 0.7701 | |

EC 1 | -0.0009 | 0.0007 | -1.2178 | 0.2254 | |

EC 2 | 0.1183 | 0.0243 | 4.8758 | <0.0001** | |

EC 3 | -0.2989 | 0.1028 | -2.9060 | 0.0043** | |

R² Adjusted | 0.2371 | ||||

Durbin-Watson | 2.1210 | ||||

Const. | 28.44 | 7.5652 | 3.7593 | 0.0003** | |

MTF lag 1 | -0.0004 | 0.0024 | -0.1783 | 0.8588 | |

MPR Lag 1 | -0.1465 | 0.2874 | -0.5098 | 0.6110 | |

CLR Lag 1 | 1.0164 | 0.4940 | 2.0574 | 0.0416** | |

NGR Lag 1 | -0.0874 | 0.0898 | -0.9732 | 0.3322 | |

NGR | CPI Lag 1 | -0.3677 | 0.1926 | -1.9091 | 0.0584* |

MoS | <0.0001 | <0.0001 | -2.9338 | 0.0039** | |

EC 1 | -0.0022 | 0.0021 | -1.0018 | 0.3182 | |

EC 2 | -0.1512 | 0.0720 | -2.0995 | 0.0376** | |

EC 3 | -0.9246 | 0.3052 | -3.0295 | 0.0029** | |

R² Adjusted | 0.1738 | ||||

Durbin-Watson | 1.9906 | ||||

Const. | -5.6804 | 6.2888 | -0.9033 | 0.3680 | |

MTF lag 1 | 0.0029 | 0.0020 | 1.4715 | 0.1435 | |

MPR Lag 1 | -0.2960 | 0.2389 | -1.2390 | 0.2175 | |

CLR Lag 1 | 0.3934 | 0.4107 | 0.9579 | 0.3398 | |

CPI | NGR Lag 1 | 0.2017 | 0.0746 | 2.7027 | 0.0078** |

CPI Lag 1 | 0.1201 | 0.1601 | 0.7500 | 0.4545 | |

MoS | <0.0001 | <0.0001 | 2.6582 | 0.0088** | |

EC 1 | -0.0052 | 0.0018 | -2.8882 | 0.0045** | |

EC 2 | 0.3082 | 0.0599 | 5.1488 | <0.0001** | |

EC 3 | -0.0204 | 0.2537 | -0.0806 | 0.9359 | |

R² Adjusted | 0.2937 | ||||

Durbin-Watson | 1.9147 |

Model | Number of Lags | ARCH-LM | Ljung-Box | ||

|---|---|---|---|---|---|

Test statistic | p-value | Test statistic | p-value | ||

MTF | 24 | 21.2111 | 0.6265 | 23.3252 | 0.5010 |

MPR | 24 | 40.1364 | 0.0607 | 36.8286 | 0.0555 |

CLR | 24 | 32.7394 | 0.19693 | 12.5243 | 0.9730 |

NGR | 24 | 19.0587 | 0.74885 | 12.5243 | 0.9730 |

CPI | 24 | 26.1727 | 0.3445 | 38.3917 | 0.0556 |

Equation | Period | MTF | MPR | CLR | NGR | CPI |

|---|---|---|---|---|---|---|

1 | 156.9700 | 0.0056 | 0.1455 | 0.0519 | -0.1071 | |

2 | 70.7130 | -0.1612 | 0.1624 | -0.3714 | -0.3611 | |

MTF | 5 | 38.5970 | -0.5779 | -0.2927 | -0.9876 | -1.4837 |

10 | 36.2690 | -0.6338 | -0.3681 | -1.2076 | -1.5084 | |

15 | 37.3690 | -0.6260 | -0.3612 | -1.1839 | -1.4939 | |

1 | 0.0000 | 2.0455 | 1.1607 | -0.5482 | 2.7623 | |

2 | 2.6250 | 1.8693 | 1.0393 | -0.5677 | 2.3329 | |

MPR | 5 | -10.0560 | 1.5268 | 0.5892 | -0.5268 | 1.3452 |

10 | -5.8614 | 1.4360 | 0.4533 | -0.4254 | 1.1072 | |

15 | -4.8469 | 1.4307 | 0.4437 | -0.3846 | 1.0806 | |

1 | 0.0000 | 0.0000 | 0.9925 | -0.5358 | 1.8101 | |

2 | 18.3370 | -0.2310 | 0.8868 | -0.0606 | 1.5367 | |

CLR | 5 | -5.0616 | -0.4242 | 0.06951 | -0.3580 | -0.0964 |

10 | 5.1160 | -0.5893 | -0.1868 | -0.1251 | -0.5341 | |

15 | 7.0816 | -0.6004 | -0.2061 | -0.0418 | -0.5900 | |

1 | 0.0000 | 0.0000 | 0.0000 | 4.4870 | -0.2061 | |

2 | 3.1975 | 0.5065 | 0.5029 | 2.7496 | 1.4239 | |

NGR | 5 | -42.6340 | 0.2461 | 0.2624 | 1.4904 | 1.1442 |

10 | -39.0450 | 0.2570 | 0.2529 | 1.3400 | 1.2778 | |

15 | -38.2300 | 0.2648 | 0.2610 | 1.3641 | 1.2897 | |

1 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 1.8330 | |

2 | -14.6140 | -0.2395 | -0.0394 | 0.1813 | 1.3721 | |

CPI | 5 | -14.1920 | -0.2578 | 0.0520 | 1.4479 | 0.7532 |

10 | -28.5910 | -0.3052 | 0.0447 | 1.2763 | 0.6200 | |

15 | -29.1320 | -0.3025 | 0.0487 | 1.2344 | 0.6449 |

Equation | Period | MTF | MPR | CLR | NGR | CPI |

|---|---|---|---|---|---|---|

1 | 100.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

MTF | 2 | 98.1232 | 0.0228 | 1.1132 | 0.0338 | 0.7070 |

5 | 87.6569 | 0.4787 | 0.8890 | 9.5319 | 1.4434 | |

9 | 70.7478 | 0.1347 | 0.3483 | 26.4205 | 2.3487 | |

10 | 71.7046 | 0.8378 | 0.7161 | 20.5787 | 6.1627 | |

15 | 63.4063 | 0.7989 | 0.8320 | 24.9234 | 10.0393 | |

1 | 0.0007 | 99.9993 | 0.0000 | 0.0000 | 0.0000 | |

2 | 0.3224 | 95.1282 | 0.6609 | 3.1781 | 0.7105 | |

MPR | 5 | 4.1032 | 89.3434 | 1.7505 | 3.1819 | 1.6209 |

10 | 8.4541 | 80.8714 | 5.8667 | 2.6333 | 2.1745 | |

15 | 9.9713 | 77.2107 | 7.7992 | 2.5438 | 2.4750 | |

1 | 0.8994 | 57.2463 | 41.2463 | 0.0000 | 0.0000 | |

2 | 1.0562 | 53.9326 | 39.3574 | 5.6193 | 0.0345 | |

CLR | 5 | 1.3926 | 75.2819 | 21.9425 | 1.3335 | 0.0495 |

10 | 0.9656 | 81.5034 | 14.6424 | 2.2763 | 0.6123 | |

15 | 13.0989 | 53.7540 | 21.9662 | 10.8911 | 0.2899 | |

1 | 0.6718 | 52.5777 | 46.7505 | 0.0000 | 0.0000 | |

2 | 1.2127 | 60.6269 | 36.2952 | 1.8591 | 0.0060 | |

NGR | 5 | 2.5121 | 57.1324 | 31.4952 | 8.7470 | 0.1133 |

10 | 9.0891 | 55.7967 | 25.0409 | 9.8311 | 0.2422 | |

15 | 13.0989 | 53.7540 | 21.9662 | 10.8911 | 0.2899 | |

1 | 0.0130 | 1.4502 | 1.3850 | 97.1518 | 0.0000 | |

CPI | 2 | 0.4887 | 2.1638 | 1.0101 | 96.2233 | 0.1141 |

5 | 4.3702 | 3.0807 | 1.3733 | 80.3274 | 10.8484 | |

10 | 12.4288 | 3.4807 | 1.2544 | 63.2874 | 19.5487 | |

15 | 16.5277 | 3.3931 | 0.9564 | 56.6463 | 22.4765 |

ADF | Augmented Dickey-Fuller Test |

AfCFTA | African Continental Free Trade Agreement |

AIC | Akaike Information Criterion |

ARCH-LM | Autoregressive Conditional Heteroscedasticity – La-Granger Multiplier |

ARDL | Autoregressive Distributed Lag |

CLR | Commercial Lending Rate |

CPI | Consumer Price Inflation |

ECOWAS | Economic Community of West African States |

ECT | Error Correction Term |

FDI | Foreign Direct Investment |

FEVD | Forecast Error Variance Decomposition |

GARCH | General Autoregressive Conditional Heteroscedasticity |

HQIC | Hannan-Quinn Information Criterion |

IRF | Impulse Response Function |

LL | Log-likelihood |

MAD | Mean Absolute Deviation |

MAPE | Mean Absolute Percentage Error |

MoS | Money Supply |

MPR | Monetary Policy Rate |

MSD | Mean Squared Deviation |

MTF | Merchandise Trade Flows |

NGR | Nominal Growth Rate |

SE | Standard Error |

SBIC | Schwarz Bayesian Information Criterion |

VAR | Vector Autoregression |

VEC | Vector Error Correction |

WTO | World Trade Organization |

| [1] | Anari, A. and Kolari, J. W. (2017). Impacts of Monetary Policy Rates on Interest and Inflation Rates. Available at SSRN 3088133. |

| [2] | Ali, T. M., Mahmood, M. T. and Bashir, T. (2015). Impact of interest rate, inflation and money supply on exchange rate volatility in Pakistan. World Applied Sciences Journal, 33(4): 620-630. |

| [3] | Asiamah, M., Ofori, D., and Afful, J. (2019). Analysis of the determinants of foreign direct investment in Ghana. Journal of Asian Business and Economic Studies, 26(1): 56-75. |

| [4] | Atimu, L. K. D., and Luo, W. (2020). Assessing domestic and regional factors influencing Ghana’s export trade in Africa. Open Journal of Business and Management, 9(1): 103-113. |

| [5] | Boamah, B. B., Assiamah, A. A., Cailou, J., Shuangqin, L., and Adu-Gyamfi, E. (2019). Factors influencing the competitiveness of cocoa export of Ghana and its implication on Ghana’s economy. Journal of Economics and Sustainable Development, 10(6): 9-46. |

| [6] |

Baum, C. F. (2013). EC 823: Applied Econometrics. Lecture notes on VAR, SVAR and VECM models. Boston College.

http://fmwww.bc.edu/EC-C/S2013/823/EC823.S2013.nn05.slides.pdf |

| [7] | Bennett, F., Lederman, D., Pienknagura, S., and Rojas, D. (2016). The volatility of international trade flows in the 21st century: Whose fault is it anyway? Policy Research Working Paper 7781. |

| [8] | Brooks, Chris (2008). Modeling Long-run relationships in finance. Chapter 8. Introductory Econometrics for Finance. Introductory Econometrics for Finance, Cambridge University Press. pp. 353 – 414. |

| [9] |

Donadelli, M., Grüning, P., and Proskute, A. (2019). Monetary policy, trade, and endogenous growth under different international financial market structures. Bank of Lithuania. No. 57.

https://www.lb.lt/uploads/publications/docs/21247_b90077d8788f25cf576f67d67871d8c4.pdf |

| [10] | Douglas C. Montgomery, Cheryl L. Jennings and Murat Kulahci (2015). Introduction to Time Series Analysis and Forecasting, Second Edition. John Wiley & Sons, Inc. |

| [11] | Feyisa, B. W. (2021). Determinants of Ethiopia's coffee bilateral trade flows: A panel gravity approach. Turkish Journal of Agriculture - Food Science and Technology, 9(1): 21–27. |

| [12] | Indrajaya, D. (2022). Relationship of Inflation, BI Rate and Deposit Interest Rate. Ekonomi, Keuangan, Investasi Dan Syariah (EKUITAS), 3(3): 401-407. |

| [13] | Krušković, B. D. (2017). Exchange rate and interest rate in the monetary policy reaction function. Journal of Central Banking Theory and Practice, 6(1): 55-86. |

| [14] |

Laksono, R. R. and Saudi, M. H. M. (2020). Analysis of the factors affecting trade balance in Indonesia. International Journal of Psychosocial Rehabilitation, 24(02): 3113 – 3120.

http://repository.widyatama.ac.id/xmlui/handle/123456789/12377 |

| [15] | Mpofu, R. T. (2011). Money supply, interest rate, exchange rate and oil price influence on inflation in South Africa. Corporate Ownership and Control, 8(3): 594-605. |

| [16] | Oboro, E. D. (2023). The dynamics of trade balance in the West African Monetary Zone (WAMZ) countries. West Africa Dynamic Journal of Humanities, Social and Management Sciences and Education, 4: 2955 – 0556. |

| [17] | Phaleng, L. T. (2020). Determinants of South Africa's fruit export performance to West Africa: A panel regression analysis. Doctoral dissertation, North-West University, South Africa. |

| [18] |

Raga, S. (2022). Ghana: Macroeconomic and trade profile: Opportunities and challenges towards implementation of AfCFTA. ODI-GIZ AfCFTA policy brief series.

https://odi.cdn.ngo/media/documents/Ghana_macroeconomic_and_trade_profile_2023_final.pdf |

| [19] | Zhong, S., and Su, B. (2023). Assessing factors driving international trade in natural resources 1995–2018. Journal of Cleaner Production, 389: 136110. |

| [20] | Stašys, R., and Tananaiko, T. (2019). Analysis of factors influencing the world trade volumes. Scientific Notes, 20: 5-17. |

| [21] | Sumani, I. I. (2015). Determinants of Ghana’s trade flows in Economic Community of West African States: Application of the gravity model. Istanbul Technical University. Retrieved from |

| [22] | World Bank (2022). Leveraging trade policy reforms to diversify and transform Ghana for better jobs. World Bank’s Publication: June 9, 2022. |

| [23] | World Trade Organization (WTO) (2022). Trade Policy Review. WTO Secretariat Ghana. |

| [24] | Yu, C. (2016). An influence factor analysis of international trade flow using a gravity model. International Journal of Simulation--Systems, Science & Technology, 17(36): 23.1 – 23.6. |

| [25] | Yeboah, E. (2018). Foreign direct investment in Ghana: The distribution among the sectors and regions. International Journal of Current Research, 10(01): 64292-64297. |

APA Style

Ibrahim, A. A., Abonongo, A. I. L. (2024). Modelling the Relationship Between Merchandise Trade Flows and Some Macroeconomic Variables in Ghana. American Journal of Theoretical and Applied Statistics, 13(5), 157-174. https://doi.org/10.11648/j.ajtas.20241305.15

ACS Style

Ibrahim, A. A.; Abonongo, A. I. L. Modelling the Relationship Between Merchandise Trade Flows and Some Macroeconomic Variables in Ghana. Am. J. Theor. Appl. Stat. 2024, 13(5), 157-174. doi: 10.11648/j.ajtas.20241305.15

AMA Style

Ibrahim AA, Abonongo AIL. Modelling the Relationship Between Merchandise Trade Flows and Some Macroeconomic Variables in Ghana. Am J Theor Appl Stat. 2024;13(5):157-174. doi: 10.11648/j.ajtas.20241305.15

@article{10.11648/j.ajtas.20241305.15,

author = {Azebre Abu Ibrahim and Anuwoje Ida Logubayom Abonongo},

title = {Modelling the Relationship Between Merchandise Trade Flows and Some Macroeconomic Variables in Ghana

},

journal = {American Journal of Theoretical and Applied Statistics},

volume = {13},

number = {5},

pages = {157-174},

doi = {10.11648/j.ajtas.20241305.15},

url = {https://doi.org/10.11648/j.ajtas.20241305.15},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajtas.20241305.15},

abstract = {Macroeconomic variables serve as economic indicators that offer valuable insights into the overall health and stability of an economy. Changes in these variables can have significant impacts on a country's trade balance and overall economic performance. This study employed multivariate time series analysis to study the relationship between Merchandise Trade Flows (MTF), Monetary Policy Rate (MPR), Commercial Lending Rate (CLR), Nominal Growth Rate (NGR) and Consumer Price Index (CPI) with Money Supply (MoS) as exogenous variable. The nature of trend in each series was investigated. The results revealed that quadratic trend model best models MTF, MPR, CLR and NGR whiles an exponential trend best models CPI. Johansen’s co-integration test with unrestricted trend performed revealed the existence of long-run equilibrium relationships between the variables and three (3) co-integrating equations described this long-run relationship. In terms of short-run relationships, the VEC (2) model revealed that, CLR, NGR, MoS have positive and significant impact on MTF. CLR, NGR and MoS have positive and significant impact on MPR, NGR have positive and significant impact on CLR, CPI and MoS have significant impact on NGR whiles NGR and MoS have significant impact on CPI. Model diagnostics performed on the VEC (2) model showed that, all the model parameters are structurally stable over time and the residuals of the individual models are free from serial correlation and conditional heteroscedasticity. Forecast error variance decomposition (FEVD) analysis showed that each variable primarily explained its own variance and the influence of other variables increase over time. Hence, adopting a broad perspective on macroeconomic variables can help policymakers anticipate and mitigate ripple effects across various economic sectors.

},

year = {2024}

}

TY - JOUR T1 - Modelling the Relationship Between Merchandise Trade Flows and Some Macroeconomic Variables in Ghana AU - Azebre Abu Ibrahim AU - Anuwoje Ida Logubayom Abonongo Y1 - 2024/10/29 PY - 2024 N1 - https://doi.org/10.11648/j.ajtas.20241305.15 DO - 10.11648/j.ajtas.20241305.15 T2 - American Journal of Theoretical and Applied Statistics JF - American Journal of Theoretical and Applied Statistics JO - American Journal of Theoretical and Applied Statistics SP - 157 EP - 174 PB - Science Publishing Group SN - 2326-9006 UR - https://doi.org/10.11648/j.ajtas.20241305.15 AB - Macroeconomic variables serve as economic indicators that offer valuable insights into the overall health and stability of an economy. Changes in these variables can have significant impacts on a country's trade balance and overall economic performance. This study employed multivariate time series analysis to study the relationship between Merchandise Trade Flows (MTF), Monetary Policy Rate (MPR), Commercial Lending Rate (CLR), Nominal Growth Rate (NGR) and Consumer Price Index (CPI) with Money Supply (MoS) as exogenous variable. The nature of trend in each series was investigated. The results revealed that quadratic trend model best models MTF, MPR, CLR and NGR whiles an exponential trend best models CPI. Johansen’s co-integration test with unrestricted trend performed revealed the existence of long-run equilibrium relationships between the variables and three (3) co-integrating equations described this long-run relationship. In terms of short-run relationships, the VEC (2) model revealed that, CLR, NGR, MoS have positive and significant impact on MTF. CLR, NGR and MoS have positive and significant impact on MPR, NGR have positive and significant impact on CLR, CPI and MoS have significant impact on NGR whiles NGR and MoS have significant impact on CPI. Model diagnostics performed on the VEC (2) model showed that, all the model parameters are structurally stable over time and the residuals of the individual models are free from serial correlation and conditional heteroscedasticity. Forecast error variance decomposition (FEVD) analysis showed that each variable primarily explained its own variance and the influence of other variables increase over time. Hence, adopting a broad perspective on macroeconomic variables can help policymakers anticipate and mitigate ripple effects across various economic sectors. VL - 13 IS - 5 ER -

Department of Statistics and Actuarial Science, School of Mathematical Sciences, C. K. Tedam University of Technology and Applied Sciences, Navrongo, Ghana

Department of Statistics and Actuarial Science, School of Mathematical Sciences, C. K. Tedam University of Technology and Applied Sciences, Navrongo, Ghana

Information